Next Mile

Next Mile

Originally published by Craig Iskowitz

“Every company will eventually be in the data business.”

Businesses are flooded with data and analytics tools promising to help them be more competitive and they need both more than ever before. As Competing on Analytics, because so many organizations offer similar products powered by similar technologies, the last remaining points of differentiation are business processes. And analytics-driven competitors will be able to squeeze every last drop of value from those processes.

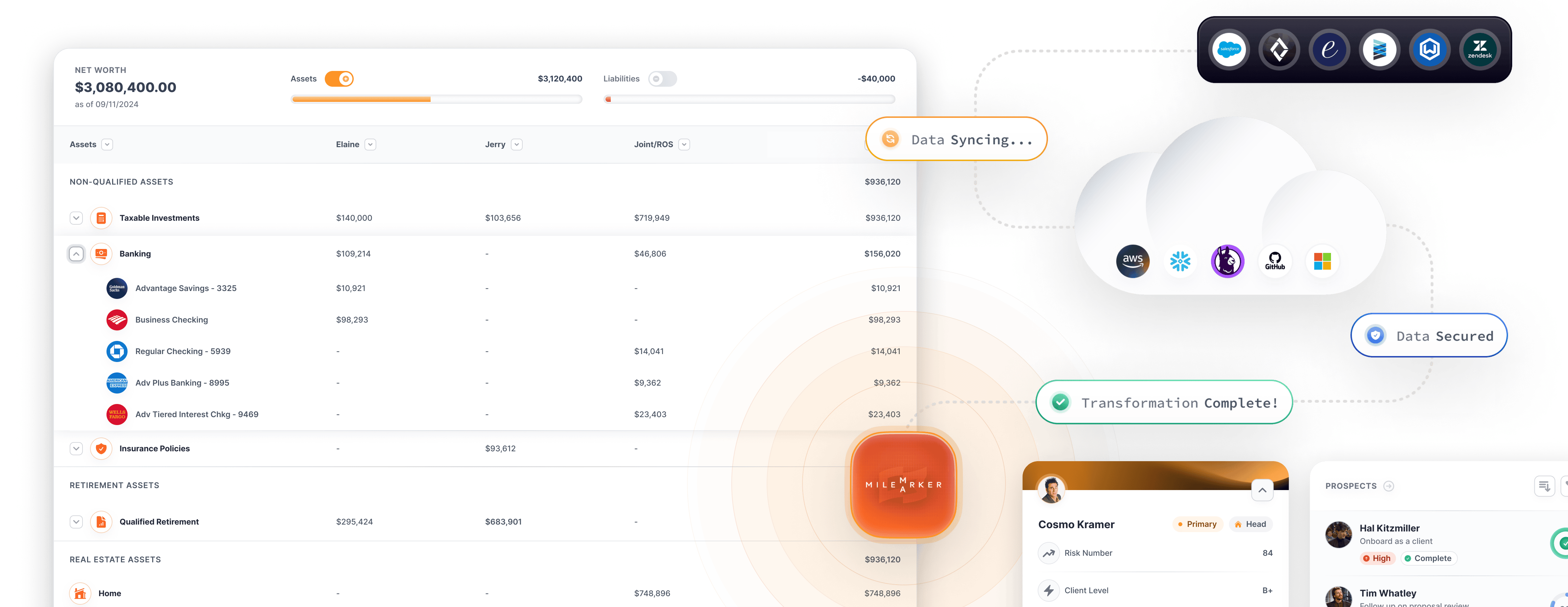

Many of the wealth management firms Ezra Group works with are facing challenges with data usage and accessibility. A study commissioned by Deloitte found that client and position data is often distributed across multiple systems and even though data warehouses may exist, it is difficult to collect and aggregate from multiple repositories and then drill down to locate insights.

Unstructured client data is especially difficult to handle in a scalable manner, which is why so many wealth management firms built data lakes to store this data. Yet they still struggle with monitoring and controlling their data, responding to regulatory inquiries, and reacting to market conditions in a timely manner.

In order for a data lake to reach its full potential, an organization must have a clear and standardized vision of all data sources. Data can be ingested in its raw form into a data lake without any processing, but once the data is stored in the data lake it needs proper cataloguing, stewardship and control to ensure data can be tracked, identified and accessed by the authorized users only (Towards Data Science).

Those companies that have overcome these issues realize that a robust and flexible data management approach is required. This approach encompasses data governance, data quality, master data management, and metadata management. Each of these capabilities are crucial to achieving data quality, consistency, and sustainability across the firm.

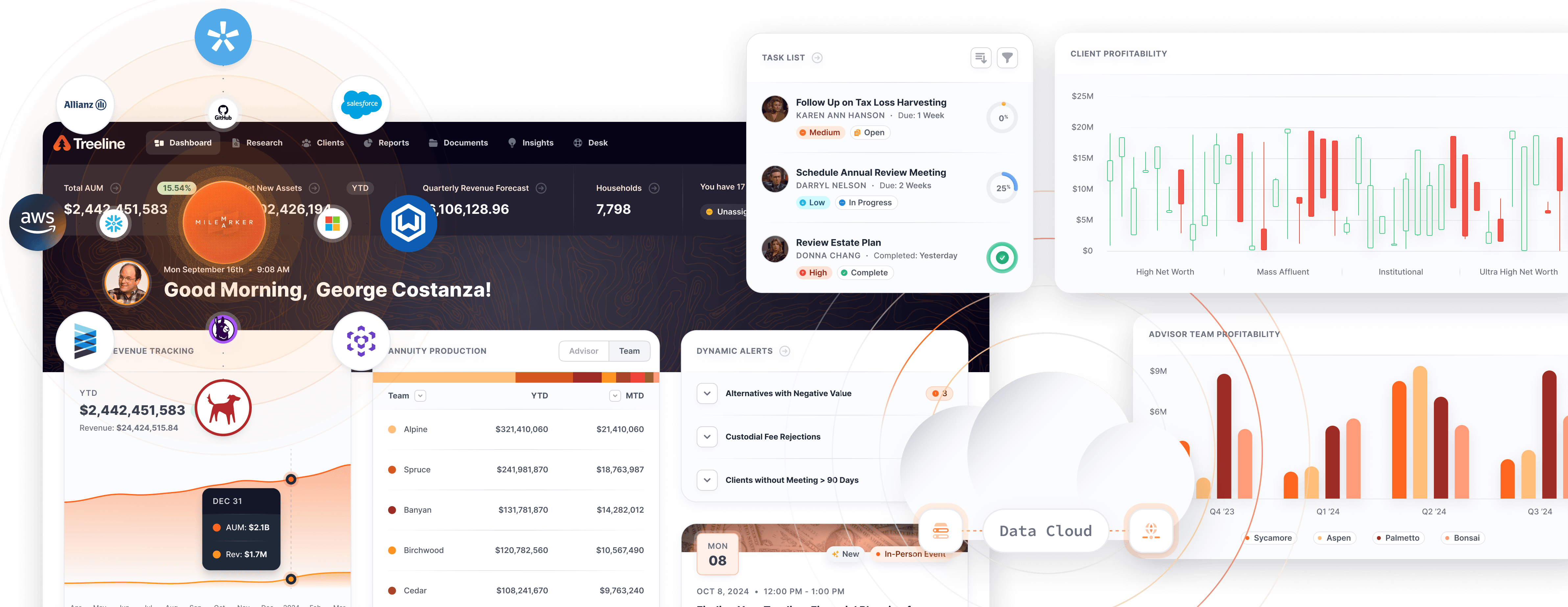

Along with our partners at Xtiva Financial Systems, we have been producing a series of webinars to bring leading industry experts in data strategy, data architecture and systems implementation to share their experiences and best practices around leverage Data-as-an-Asset for enterprise wealth management firms.

Our most recent webinar, called The Data Engines Powering Wealth Management, included panelist Jud Mackrill, CEO and Co-Founder of Milemarker, who shared some best practices when working with vast amounts of client data and offered advice on how to deal with it effectively.

In case you missed this webinar, click here to unlock your access to the full recording.

Expansion of APIs Across Wealth Management

“The expansion of #APIs across #wealthmanagement technology enables firms to develop #clientexperience that aligns more closely with optimal human behavior.”

— Jud Mackrill

“Design is not just what it looks like and feels like. Design is how it works.”

— Steve Jobs

Any construction engineer worth their salt would say that you need to build on a solid foundation if you don’t want your building to collapse. The same holds true for APIs. If you haven’t done a good job in designing the API framework, it will have cascading effects on other parts of your software development.

APIs are starting to look more like a product in their own right rather than just a technology. They should be seen as a way to deliver functionality to your end users.

According to Paul Jacobs, Deloitte’s Customer Experience Transformation Director, a truly great customer experience means providing a better service than what the customer can do themselves using these technologies. Unfortunately, as businesses try to keep up with the technologies customers are using, they tend to generate more silos and isolated customer data. This leads to disconnected and ultimately negative customer experiences.

“Businesses are focusing intently on individual touchpoints, rather than looking at the end-to-end journey,” says Jacobs. “This only serves to reinforce the silos in their business and drive a disconnected customer experience.” The secret to breaking down the silos and transforming the customer experience is developing an API strategy.

Organizations need to develop new “muscle memory” when revamping #datastrategy, tips from Sprint by @jakek — @JudMackrill @MilemarkerData

Building Custom Client Experiences

“Wealth management firms will be able to make their own “mix tape” of data that is most valuable to them no matter the source system.”

— Jud Mackrill

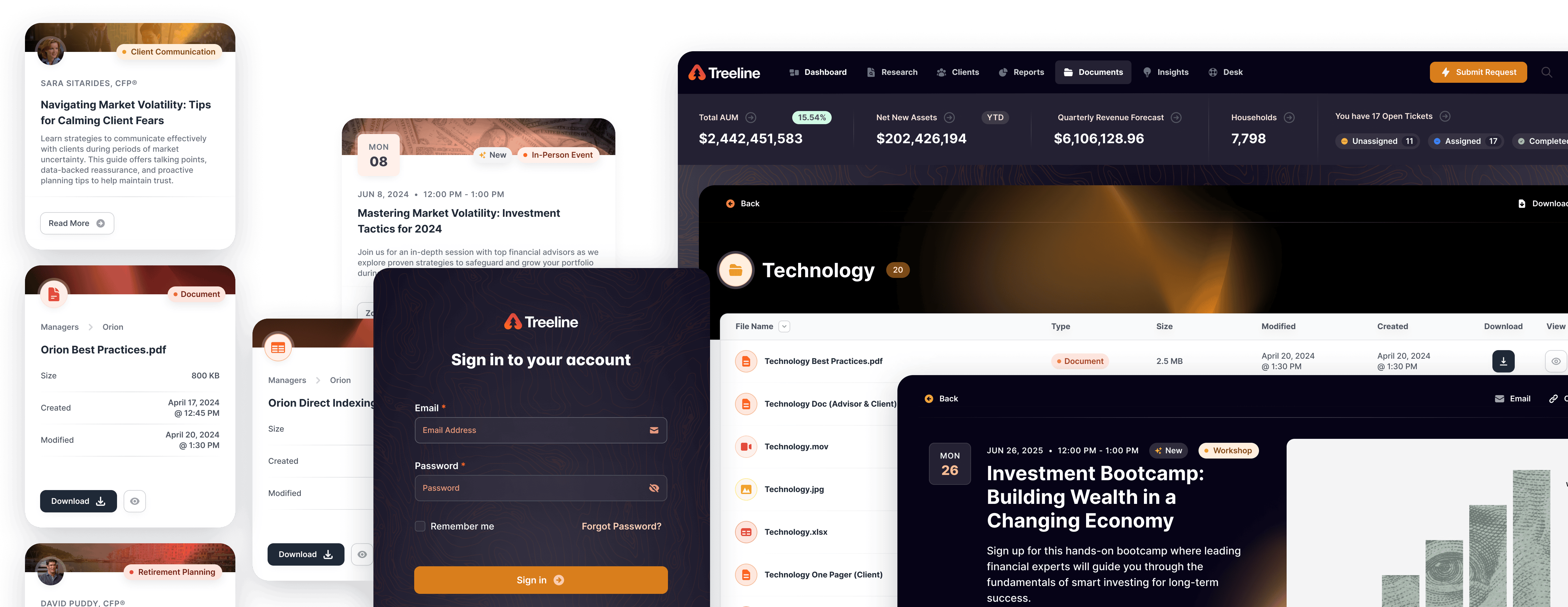

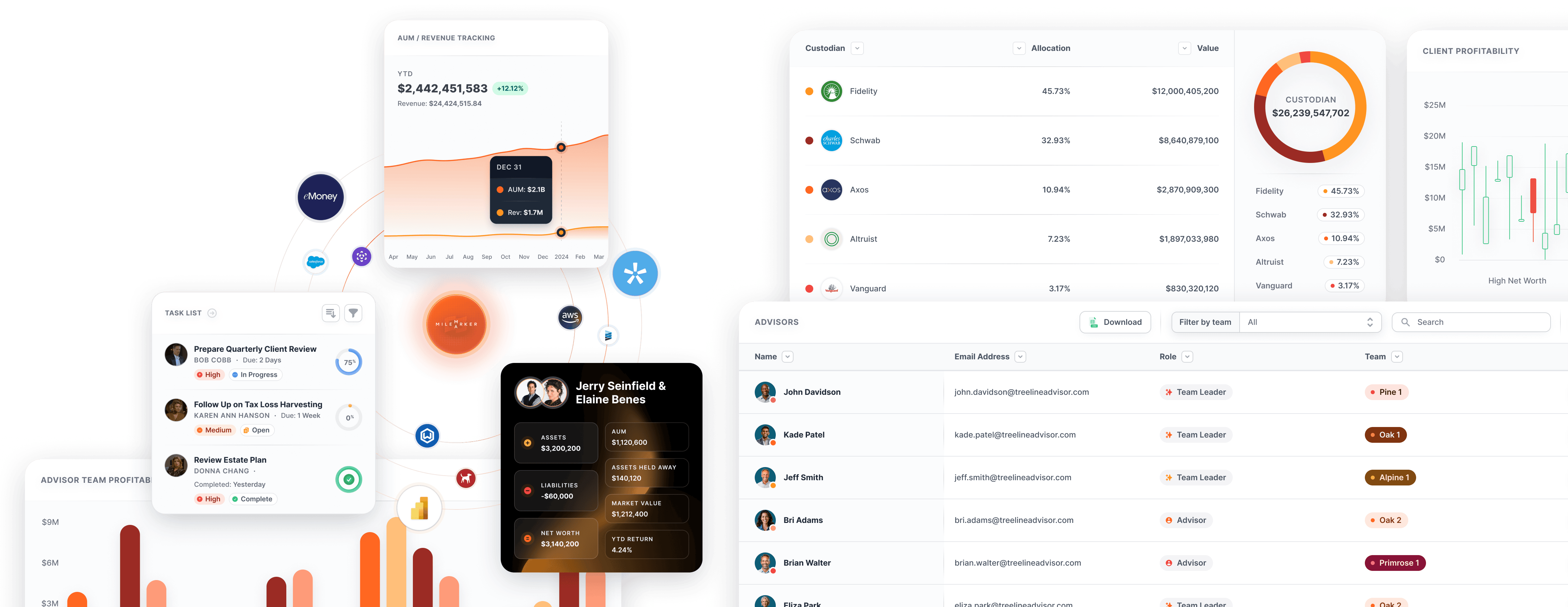

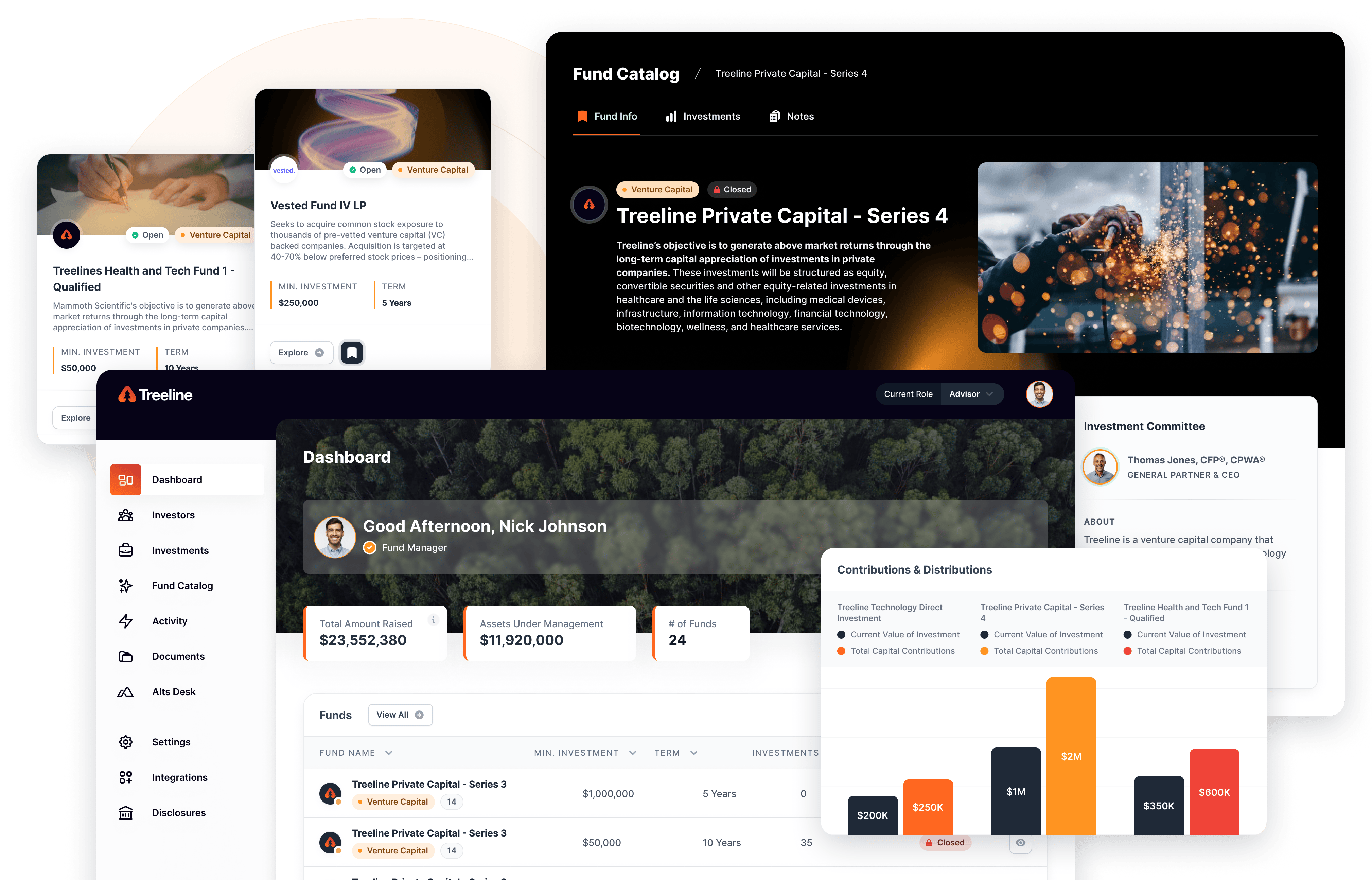

The growing number of interfaces made available between vendors and the amount of data provided is enabling more wealth management firms to build their own custom tools, reporting and overlay experiences for advisors. The largest broker-dealers have built their own advisor platforms, usually on top of an application framework provided by one of the larger technology vendors.

LPL Financial, Advisor Group, Cetera, Commonwealth and others have highly customized systems that they have invested extensive resources to build. But the cost of building software and connecting to data sources has dropped to the point where even the smallest firms are able hire a programmer or two or contract with an outsourcer to build new tools and user interfaces.

This can make their ecosystems less complex if they are able to design their new UI/UX in such a way as to be easier to navigate and focus advisors on exactly what they need to get done. Utilizing the out-of-the-box screens from a major vendor can be difficult and require extensive training since they were built to be generic to appeal to the widest audience.

Demand for APIs from Pershing clients has increased 2-3X year-over-year, according to Lee. This is transformational as wealth management firms combine data from multiple sources into a more holistic view of client financial lives, she said.

Occasionally these internally-developed systems become so robust that they can be sold to other broker-dealer and become products in their own right. Commonwealth Financial Network spun off their platform into a company called Advisor360 to offer their highly-rated advisor software to other wealth management firms. Insurer MassMutual and its 9,000-broker IBD reached the first licensing agreement with the new firm back in 2019.

Vertically Integrated Systems

Vertically integrated systems are more resilient compared to horizontally integrated ones that are only as reliable as the weakest link.

— Jud Mackrill

Investopedia explains the differences between horizontal and vertical integration as:

- A horizontal acquisition is a business strategy where one company takes over another that operates at the same level in an industry.

- Vertical integration involves the acquisition of business operations within the same production vertical.

- Horizontal integrations help companies expand in size, diversify product offerings, reduce competition, and expand into new markets.

- Vertical integrations can help boost profit and allow companies more immediate access to consumers.

- Companies that seek to strengthen their positions in the market and enhance their production or distribution stage use horizontal integration.

For example, Envestnet’s 2017 acquisition of Foliodynamix was an example of horizontal integration, since they operated in the same space with overlapping wealth management platforms. However, Envestnet’s 2015 acquisition of Yodlee was a vertical integration play since Yodlee offered data aggregation services, which are complimentary and can provide data to the wealth management platform.

A white paper from McKinsey recommends vertical integration when it would create or exploit market power by raising barriers to entry or allowing price discrimination across customer segments. Envestnet buying Yodlee had the potential to deliver this if they can tightly integrate the new data services to feed analytics and reporting that competitors cannot match.

Why You Should Drain Your Data Lake

Data Strategy Tip: 85% of Big Data projects fail. Instead start slowly by building a data warehouse first.

— Jud Mackrill

One of the key decisions wealth management CTOs and CIOs face today is where to store all of their company’s data, as described by George Fraser, CEO of automated data integration provider Fivetran:

For the last 10 years, many enterprises have answered this question with a two-pronged approach: First, they spin up a data lake using Hadoop or Amazon S3, which acts as a storage repository for all the raw data — both structured and unstructured — no matter the purpose. Basically, it’s a place to park data before deciding what to do with it. Then, they deploy a traditional data warehouse, such as Teradata, Vertica or Netezza. Data warehouses store curated data — that is, data that is filtered and processed for a specific purpose.

During our pre-game discussions, the panelists all had some strong negative opinions about data lakes, with Mackrill being the most vocal. He noted that even though we live in a very structured world, data lakes are unstructured and he questioned the value received from unstructured data in our space when 85% of big data projects are failures.

Mackrill recommended that wealth management firms avoid a two-tier system and consider whether they need both a data lake and a data warehouse — or if they can simplify their architecture by using the same physical system for both.

Instead, just build the data warehouse. As cloud-based storage rates continue to fall, there’s no longer a cost benefit to splitting your data between a data warehouse, which used to be expensive, and a data lake, which used to be cheaper.

After getting a data warehouse, firms should create their own organizational schema and then start building solutions off of that instead of jumping head first into a Lake, without a proverbial “life preserver,” Mackrill advised.